Mark Hulbert recently published an ominous warning at

MarketWatch about excessive valuation in the U.S. equity market. Most valuation ratios are in the top 90% since 2000 and “as overvalued as it was at the market top on Jan. 3, 2022”.

How worried should you be?

Hulbert admitted in his article that “valuation has relatively little predictive power at shorter-term horizons”. Take, for instance, the forward P/E ratio. While the S&P 500 forward P/E is at similar levels as the market top in early 2022, it was higher and for a prolonged period for nearly two years before the top and stock prices kept on rising during that time.

When valuation and value matters

While valuation doesn’t matter much in the short run, Hulbert pointed out that “each of the indicators featured in the chart has an impressive record forecasting the stock market’s return over the subsequent decade”.

If valuation only matters in the long run, it follows that value investing has to be a patient discipline. This analysis from

GMO argues that only deep value stocks are cheap. Even shallow value is at the top 80% of historical norms, while deep value is in the bottom 10%.

If GMO is correct and only deep value is cheap, what if I told you I have a quantitative screen that found a group of companies with strong balance sheets, strong cash flows and trading at a median forward P/E of 11?

Insights from LBO modeling

I first wrote about leveraged buyouts, or LBOs, in May (see How To Buy A Company If You Have No Money). Here is how my LBO model works. First, you eliminate financial companies from consideration because these companies already have highly leveraged balance sheets and you can’t LBO a bank or insurance company. The way you LBO a company is to pay equity holders with the company’s own money.

LBO value = Cash + Extra borrowing power

Where

Extra borrowing power = Allowable borrowing power – Existing debt – Leasehold obligations

To calculate allowing borrowing power, I calculated the 5-year standard deviation of EBITDA margin divided by median EBITDA margin as a measure of the underlying volatility of the business. I then divided the results into deciles. The most volatile decile was assigned an allowable EBITDA interest coverage of six and least volatile an allowable interest coverage of two. From that:

Allowable borrowing power = EBITDA / Allowable interest coverage / Financing rate

While it is said that growth stocks are highly rate sensitive because they are long-duration assets, so are LBO stocks.

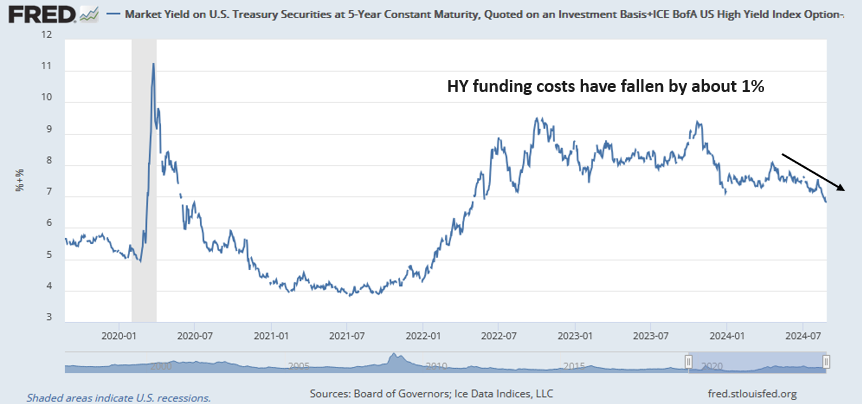

Here is what’s happened since my initial publication in May. I screened the non-financial stocks in the S&P 1500 using my LBO criteria. There are only 10 stocks that you could buy with no money down. But if I relaxed the criteria to 30% down, the number of stocks that passed my screen rose dramatically from 25 in the last month to 40. Most of the increase is attributable to falling junk bond yields, as proxied by the 5-year Treasury yield + High Yield spread. Funding costs for junk bonds have fallen by about 1% since I began this study.

As LBO candidates tend to be deep value stocks, investors will need to exercise some patience with these names. As one of several examples, coal stocks, which are in a hated industry, have begun to appear as LBO candidates owing to the beaten up valuation and cash flows.

SunCoke is a producer of coking coal that is statistically cheap, but investors may need to be patient with the stock in light of widespread steel overcapacity in China, which has also been reflected in weakness in the price of iron ore.

To be sure, there were some unusual quick successes. I identified the old dot-com darling Cisco Systems as a possible LBO candidate at the height of the early August panic (see

What Will Lead the Expected Market Rebound?). The stock rallied soon afterwards on a strong earnings report.

In conclusion, the stock market appears to be overvalued by a number of metrics, valuation doesn’t matter over the short term, but they are predictive of long-term returns. Deep value stocks in the U.S. are still cheap. My list of LBO candidates, which tend to have strong cash positions, strong balance sheets and cash flows, represent a pocket of deep value. In particular, the retreat in junk bond yields has made these stocks even more attractive as investments.

However, many of the stocks identified by the LBO screen are blemished, each in a different way. A deep value screen like the LBO should be used by investors to identify stocks for further detailed fundamental analysis as there is a heightened risk of value traps in many of the names. This is not a quantitative factor that can be blindly bought because of the high degree of stock-specific risk which will be difficult to diversify away.

The list of LBO stocks that passed my screen is a specialized report designed for institutional investors. Readers who would like to see a full list should contact Ed Pennock at ed@pennockideahub.com.

“Translated, stock picking matters in the middle of the valuation distribution matters less (shallow growth and value) because of indexing.”

What?

Translated, stock picking matters. But in the middle of the valuation distribution, it matters less (shallow growth and value) because of indexing.

Hi Cam, any examples of ETFs that focus on deep value? Thanks

I am unaware of any deep value ETFs. You’ll have to look at individual managers. While this isn’t a recommendation, GMO has a set of mutual funds

https://www.gmo.com/americas/investment-capabilities/mutual-funds/?asset_class=905e3bb9-d230-437f-94a3-44da1562c08c

Thank you!

The most important word there is “patient”

One can ash “Why is it a value stock?”. Well, because it is out of favor, for whatever reason. It may stay out of favor for a long time. How long will esg last?

Coal, cigarettes, oil , they all take a hit.

If a stock is out of favor retail won’t chase it so Wall Street won’t be able to take our money away from us. This means that it is unlikely to make moves like the glamor tech stocks, no dopamine hit.

I remember stocks that were making money with a P/E of 3 back in the 70s.

There is no telling how much of a change there will be in the coming years, but for us longs , I hope the overvaluation continues, which of course is unlikely.

Stock picking or at least sector picking appeals to a Luddite like me. Just tossing money into an index fund is for the millennials. Apologies to them.