Preface: Explaining our market timing models

The latest signals of each model are as follows:

- Ultimate market timing model: Buy equities (Last changed from “sell” on 28-Jul-2023)

- Trend Model signal: Bullish (Last changed from “neutral” on 28-Jul-2023)

- Trading model: Neutral (Last changed from “bullish” on 23-May-2024)

Update schedule: I generally update model readings on my site on weekends. I am also on X/Twitter at @humblestudent. Subscribers receive real-time alerts of trading model changes, and a hypothetical trading record of those email alerts is shown here.

Subscribers can access the latest signal in real time here.

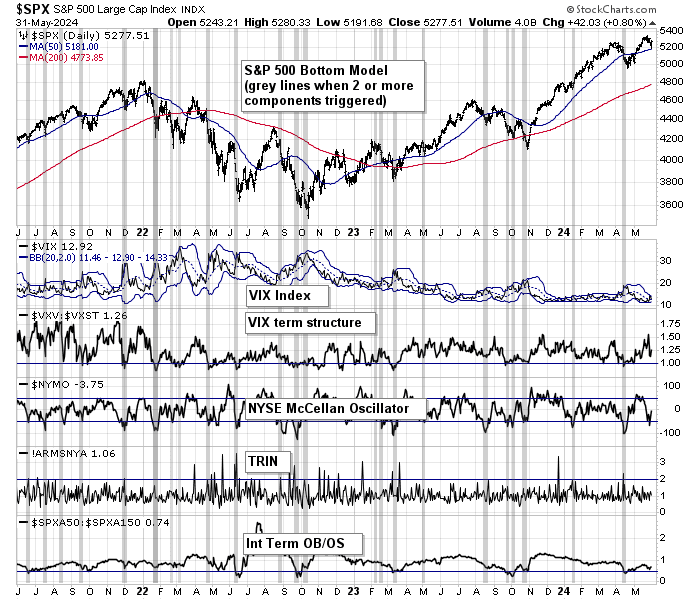

A failed breadth thrust?

On the other hand, the short-term warning signs have been appearing everywhere. Even as the S&P 500 advanced to new all-time highs, the 5-week RSI flashed a negative divergence, and so did the VVIX/VIX ratio.

Is this evidence of a failed breadth thrust? How should investors react to the simultaneous appearance of bullish price momentum signals like a breadth thrust and the risk of dips from negative technical divergences?

Warning signals

The warning signs were plain to see. I highlighted the excessive bullishness of the put/call ratio last week.

Moreover, the daily S&P 500 chart was flashing warning signs. It’s not unusual for the index to consolidate sideways for a few days after reaching its upper Bollinger Band before making the next directional move. The latest move was foreshadowed by a bearish recycle of the stochastic from overbought to neutral. However, the market did show a constructive reversal candle on Friday, which needs to be confirmed by bullish follow through next week.

Limited downside risk

The Zweig Breadth Thrust Indicator, which is reported with a delay, came within a hair of an oversold condition last week, and its real-time estimate did become oversold, though that does not count as an “official” oversold reading. In the past, the market has bottomed soon after similar episodes.

As well, one of the important indicators of equity risk appetite, which was bearish last week, is turning up. The relative performance of equal-weighted consumer discretionary may be bottoming, which is a constructive sign.

Key risk

Notwithstanding the softer-than-expected core PCE report that depressed bond yields, auction supply is expected to rise and peak in June. This will put additional pressure on yields in the new month and present a key test for risk appetite. {Corrected chart below)

In conclusion, I believe the bullish implication of Triple 70 Breadth Thrust triggered on May 6 is still alive. The U.S. equity market has just hit a temporary air pocket and should experience a shallow pullback. The key risk is how the bond market reacts to a continuing flood of issuance in June, which could put upward pressure on yields and downward pressure on risk appetite.

More anecdotes for average Joes. Memorial Day weekend movie box office 2024 is the slowest in 30 years, without factoring in inflation. Cruises are starting to offer discounts, as opposed to rosy reports in the media. So consumers are getting more discretionary and selective. I run my own search engines trying to detect the mood of average serfs in America and plot the time series. What I found is that more and more ordinary Americans are fed up and ready to give up. Let’s see what Q2 GDP looks like in a few months. Obviously the way America is being run is not sustainable, based on observations. And the distrust of US gov data is steadily rising. There is a big gap between how average people face/experience and what gov data depict. On the other end of the spectrum people are happy with their financial situation and optimistic about the future. But they are getting cautious. Walmart management has mentioned this point in their latest earnings report.

Things can obviously improve. Let’s continue to observe. But the reality is that the problem is becoming structural. It is getting more and more difficult to solve without some sort of pain and expectation adjustment.

Since I am a short term momentum trader I place a great emphasis on technical analysis and indicators. However, I am cognizant of the fact that it is not the be all and end all. Case in point what we are presently seeing is both parties not make any attempt to address the fiscal deficit.

In fact, it is just the opposite. We will see taxes reduced if Trump gets elected and Biden will continue to spend money on unwinnable wars. If this scenario holds we are going to continue to see a back up in yields with a slowing economy. The Fed cannot do much on the long end of the yield curve. High interest rates and a likely recession – not a pretty picture.