A recent comment by Michael Mauboussin of Credit Suisse that nailed the dilemma of active managers, namely that using traditional approaches to alpha generation is akin to mining lower and lower grade ore:

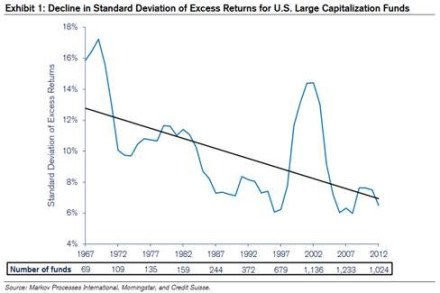

Exhibit 1 shows that the standard deviation of excess returns has trended lower for U.S. large capitalization mutual funds over the past five decades. The exhibit shows the five-year, rolling standard deviation of excess returns for all funds that existed at that time. This also fits with the story of declining variance in skill along with steady variance in luck. These analyses introduce the possibility that the aggregate amount of available alpha—a measure of risk-adjusted excess returns—has been shrinking over time as investors have become more skillful. Investing is a zero- sum game in the sense that one investor’s outperformance of a benchmark must match another investor’s underperformance. Add in the fact that in aggregate investors earn a rate of return less than that of the market as a consequence of fees, and the challenge for active managers becomes clear.

I got into quantitative investing back in the 1980`s when ideas and models were fresh and plentiful. Today, factor investing has become increasingly mainstream, and so-called “smart beta” may have exceeded their best before date.

Smart beta a crowded trade?

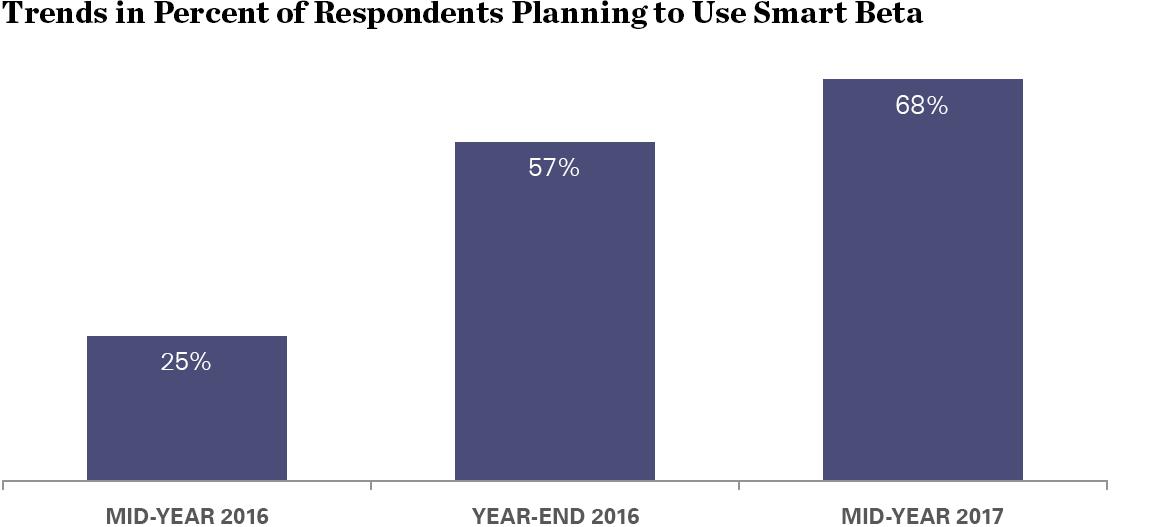

A market study by State Street Global Advisors tells the story. In this era of a shift towards passive investing, smart beta strategies have become more popular as a substitute for many investors. In the space of a year, the number of SSgA survey respondents who plan to use “smart beta” strategies surged from 25% to 68%.

|

| Source: State Street Global Advisors’ “2017 Mid-Year Survey,” as of 5/2017 |

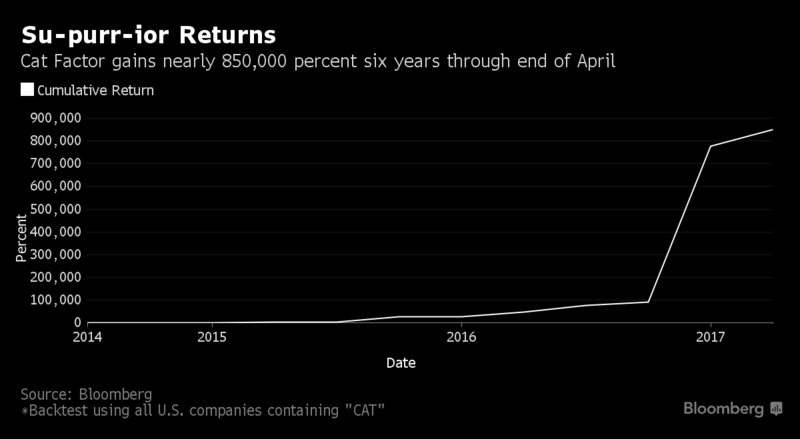

Today, the barriers to entry to factor based investing has disappeared. Investment technology has become so ubiquitous that virtually anyone could come up with a smart beta strategy. Bloomberg documented how Dani Burger created a factor which returned an astounding 849,751% return:

This is the story of the time I designed my own factor fund as a way of learning about one of Wall Street’s hottest trends — and its pitfalls. There are already ETFs that focus on themes, such as “biblically responsible” companies or ones popular with millennials. Quants have hundreds of style tilts, and their exploding popularity has created a gold rush for creators. I wanted in.

I notified Andrew Ang, head of factor investing strategies at BlackRock Inc. Everything in my program was by the book, I assured him. It was rules-based, equal-weighted and premised on a simple story — that people love cats.

How did she create her factor?

My model buys any U.S. company with “cat” in it, like CATerpillar, or when “communiCATion” is in the name. It rebalances quarterly to keep trading costs low. That’s important for when Vanguard or BlackRock license it and charge a competitively low fee.

Of course, the first iteration of buying stocks that began with “Cat” didn’t work very well, so she tweaked the results, again, and again.

She eventually got it right, and got astounding returns to her factor that we see today. While the exercise was tongue in cheek, it does illustrate the point that there are many, many quantitative researchers testing a zillion factors that sound good, but suffer from a case of torturing the data until it talks. Burger got the last word from Cliff Asness of AQR:

Like any enterprising quant, I decided to get another opinion. For this, I conferred with Cliff Asness, founder of AQR Capital Management and a pioneer of factor investing.

“Everything you can sort on can be a factor, but not all factors are interesting. Factors need some economics, theory or intuition even, to be at all interesting to us. Thus the cat factor fails as we have no story for why it should matter at all,” Asness said. “Now, in contrast, we are active traders of the dog and parakeet factors, which are based on hard neo-classical economics married to behavioral finance and machine learning. But the cat factor is just silly.”

He’s got a point. Seems like the tail risks here might be a little high.

The perils of data mining

The combination of a surge in the popularity of smart beta funds and the problems of factor backtesting is indicative of a crowded trade in many bottom-up quantitative factor strategies. Good quant factors need pass several tests:

- The factor needs an economic or market-based rationale and intuitive, such as value stocks with low P/E ratios are indicative of investor fear about a company’s outlook.

- The factor needs to be implementable. A lot of the early research uncovered factors with excess returns, but much of the alpha was in micro-cap stocks that could not be traded in reasonable size.

- The factor needs to pass the Watergate test of “what did you know and when did you know it”? Many researchers do not build in sufficient time lags into their backtests. Consequently, backtest results can suffer from a lookahead bias in their data. In addition, some companies have been known to re-state financial results. Did the backtest use the financials that were reported were reported at time, or the re-stated figures?

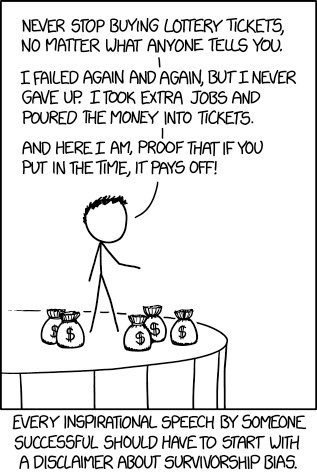

- The backtest database does not suffer from survivorship bias. Survivorship bias is the bane of quantitative researchers. I once worked at a hedge fund where a trader’s backtest assumed that companies never went bankrupt. His strategy had shown stellar results, until he bought Enron all the way down to zero. Notwithstanding obvious errors like that, the problem of dead and merged companies is a non-trivial one in financial databases. Consider the history of Time Warner, which began as Time Inc. and Warner Communications. Starting from the 1980’s, this company had bought, sold or spun off Atari, Time-Warner Communications, Turner Broadcasting, Six Flags, AOL, Time Warner Cable, and so on. Were all of these companies in the backtest database, all at right times?

It’s the hidden survivorship bias that can torpedo quantitative factor, or smart beta, strategies.

My belief about the demise of excess returns by money managers is that we are in an era when their considerable expertise no longer works like it did before. The digital revolution is such a new factor that is overwhelming the economy and business.

A great example is Walmart. Pre-digital revolution, we had business cycles where consumer spending went up and down somewhat as the economy went through booms and busts. When a bust was in play, value managers bought Walmart at a cheap price and later sold it or trimmed when it went too high in relation to historic valuation. The retail landscape was basically the same cycle on cycle (of course Walmart’s big box methods were eating up small rivals) and it was just the retail business cycle that had to be timed along with Walmart’s valuation compared to historic norms.

Today, Amazon.com and other internet related retail companies are totally transforming the retail business. A value manager can’t justify buying Amazon. How can they factor in a total disruption of an industry. I’m in oil country and technology is turning it upside down too. Industry after industry are going through disruption.

Historic cycles and previous experience are no guide in this new era. In fact, the more experience and success one has had in the past, the less likely you will adapt to new realities.

The new Central Bank QE experiment with negative interest rates and huge Central Bank balance sheets is another new factor that is confounding fixed income money managers that had a history of excess returns. Every year for the last five, fixed income managers have forecast a big rise in rates back towards some old normal and they are always wrong. Once again, previous experience is no help in this new era, it is a hindrance.

So how does one navigate this uncharted future? I’m doing it successfully with momentum-style investing. It keeps you mathematically on the right side of a changing unknowable investment landscape. Buy my book The Pathway… Your money in a time of change. The PDF eBook version is here. There is also a preview of the first part of the book there to check out before you buy.

http://thepathway.ca/

It is also on Amazon.com and Chapters/Indigo for KOBO and Kindle users.