Some minor buzz has arisen among finance academics and professionals as a result of a paper by Ronald Kahn and Michael Lemmon, both of whom are employed by Blackrock, entitled The Asset Manager’s Dilemma: How Smart Beta Is Disrupting the Investment Management Industry. Here is the abstract:

Smart beta products are a disruptive financial innovation with the potential to significantly affect the business of traditional active management. They provide an important component of active management via simple, transparent, rules-based portfolios delivered at lower fees. They clarify that what investors need from their active managers is pure alpha—returns beyond those from static exposures to smart beta factors. To effectively position themselves for this evolution in active management, asset managers need to understand the mix of smart beta and pure alpha in their products, as well as their comparative advantages relative to competitors in delivering these important components.

As Blackrock is a supplier of “smart beta” fund products, are these authors talking their own book or is this truly a new form of financial disruption?

A history lesson

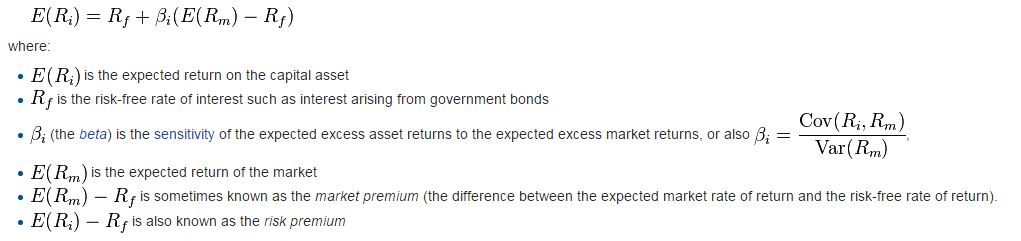

To truly understand the underpinnings of “smart beta”, we begin with a history lesson, starting with the advent of the Capital Asset Pricing Model (CAPM). According to Wikipedia, Treynor and Sharpe formulated CAPM to explain stock returns this way:

In plain English, CAPM explains the sensitivity of a well-diversified stock portfolio by its beta. In an era when investment professionals just picked stocks, CAPM was an enormous leap forward in financial innovation. Portfolio managers suddenly had a dial called beta. If you were bullish on the market, all you had to do was raise the beta on the portfolio. Conversely, if you were bearish, you could become more defensive by reducing portfolio beta.

In the wake of CAPM innovation and its sister theory, the Efficient Market Hypothesis (EMH) which postulated that you couldn’t beat the market, great controversies erupted. Throughout the 1970s, academics found a number of “market anomalies” such as market capitalization (small cap), value anomalies such as low PE and low PB. Well-diversified (underline the words well-diversified) portfolios using these techniques did in fact beat the market.

There were further problems with CAPM that led to the financial theory behind smart beta. Imagine that you formed two well-diversified portfolios with similar betas, the first composed of oil stocks and the second composed of airline stocks. We know that these two portfolios will behave very differently in the face of an oil shock, which is contrary to the expectations specified by CAPM.

Stephen Ross formulated the Arbitrage Pricing Theory (APT) by decomposing market beta in CAPM into a number of unspecified factor betas. Portfolio returns could be explained by a portfolio`s sensitivity to different factor betas, such as different sectors, or macro sensitivity such as interest rates, housing starts, inflationary expectations and so on.

Thus, factor investing was born.

Fabozzi on factor investing

CFA candidates are well aware of Frank Fabozzi, who is now a professor at EDHEC Business School. In a recent interview, Fabozzi described factor investing this way:

The belief is that if you invest in factors, you can either provide a return in the long term that will be in excess of the return on a capitalization-weighted index, or provide a better diversification format.

So which is it? Is factor investing better diversification (better beta) or a way of beating the market (alpha)? Fabozzi went on:

So that`s where it stands right now for factor-based investing strategies. They can still be active or passive strategies, but the search is still for things such as are there factors that continue to provide a risk premium over time – and that will always be an empirical issue. Some market participants talk about pure factors. What they really mean is time-tested factors that have delivered a risk premium…

…And it`s an empirical challenge; there is no underlying theory about these factors. There are economic reasons or behavioral finance reasons why you might expect a factor to be rewarded. Behavioral finance theorists do a very good job of explaining that link, but the empirical work will go on.

In other words, these factors seem to work, but nobody can really explain why.

1980s technology in a new package

Cam here. Let me explain how I once used factors as a quantitative portfolio manager to pick stocks. We would combine different uncorrelated factors, such as growth and value, to engineer a stock selection process. Further, we would selectively turn factors off and on by sector. For example, a factor like low PE may work reasonably well in a sector grouping like banks, but you would not use it to pick technology stocks because low PE technology tended to be markers for the busted growth companies that have lost their competitive position. On the other hand, a momentum or growth factor like estimate revision is probably appropriate for most sectors.

These are the kinds of techniques that quants have been using since the 1970s and 1980s to pick stocks. Today, factor investing techniques are easily accessible. Everyone has the same databases. They all look at the same factors, though the formulations are slightly different.

Blackrock et al has just re-packaged factor investing as “smart beta” as a way to sell funds. While some of these factors can and do work over time (so does “value”, “growth” and “momentum”), but they don’t work all the time and investors may have to exercise a great deal of patience (see Where I am finding value in today’s market).

The true financial innovation does not come from the factor investing technique, which is well know. Rather, itcomes from how factor investing is marketed. That’s because this marketing technique absolves the portfolio manager from poor performance. The Kahn and Lemmon paper states:

Smart beta products change the division of responsibility between investor and manager. An investor can fire an active manager who underperforms the cap-weighted benchmark over time. The investor is responsible for hiring the manager, and the manager is responsible for outperforming the benchmark. But an investor should not fire a smart-beta manager who delivers the promised exposures if those exposures lead to underperformance. The investor, not the manager, is responsible for the choice of those exposures.

In other words, you, the investor, takes all the risks for picking the factor, or “smart beta” that the fund company peddled to you. Heads they win and tails they win.

Is this financial innovation and disruption? It is, but only for the fund companies.

Good one Cam, Thanks!

As a former employee of a smart beta company, I have a slightly nuanced take on this. The original smart beta products were not called smart beta, but were marketed as an alternative way to construct a Beta 1 portfolio. PRF is an good example. PRF is not constructed via factor analysis, but by an alternative weighting scheme. The equal weighted RSP is another example. These portfolios contain factor tilts by definition, they are not cap-weighted. RSP is always going to be tilted towards small cap, value, and which ever sector/industry contains more stocks inside the S&P 500. PRF has dynamic tilts based which factors are under priced via its model.

The latter generations of “smart beta” took the marking of the previous generation and said, “we’ll just give you factors, you choose how much of each to put in your portfolio.” It is these products discussed here. To that end, I don’t see that factor based smart beta strategies absolve portfolio constructors, just give them a menu to choose from.

The earlier generations allowed you to dynamically tilt your portfolio and were sold as a replacement to a pure cap weighted index. It’s these products that I view as the replacement for active management at a low cost (assuming you believe their model).

Of course it is not as cut and dry as that. There are new products today that look more like the early generations and some old products that look like the new generation. My point remains, smart beta and factor investing are not interchangeable. Factor investing is a subset of smart beta, but not the whole.

Thanks for shedding some light on this issue. As I recall, some of the early funds were in fact a form of value factor tilt, e.g. sales weighting = sales factor.

Please tell me this (and I am not trying to be adversarial, just information gathering): With an equal weighted index, which is also implicitly a form of small cap tilt, what advantages can you cite over the cap/float weighted index? An equal weighted fund will need periodic rebalancing, which involves trading costs (and also an anti-momentum bet of selling winners and buying losers). By contrast, a cap/float weighted index needs no trading outside of changes in index constituents. Surely, you had to be able to cite some advantages in order to sell the superiority of such a weighting scheme.

Hi Cam, very good points. Research Affiliates have written a number of papers on the topic (http://www.researchaffiliates.com/Search/Pages/Results.aspx?k=rebalancing%20cost). They look at different strategies and compare market impact costs of different strategies. Equal weight does not come out well (probably obvious since Research Affiliates do not market EW strategies).

As you say, these trades are anti-momentum by construction. Some rebalancing strategies such as only rebalancing 1/N of the portfolio N times a year help to address this.

Of course, there is also the argument of a rebalancing premium. Cambell Harvey (et al) make an argument that rebalancing is a source of risk for which you do receive compensation (http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2488552). Intech is a big proponent of rebalancing and have written a great deal about it (https://www.intechjanus.com/intech/insight-and-research).

Interestingly, FTSE just put out a white paper that hits some of the same points I made — namely the distinction between type of Smart Beta, and the dynamic factor tilting of the alternative weighting category.

http://www.ftserussell.com/sites/default/files/research/alternatively_weighted_and_factor_indexes_final_revised.pdf

Dominic talked about the sophisticated things they were doing some time ago. Let me say that right now, factor investing is taking a huge step forward as the largest hedge funds that are now using artificial intelligence. Ray Dalio’s Bridgewater Associates for one is programming IBM’s Watson program for investing. This is the program that defeated the best Jeopardy champions by instantaneously scouring the internet for information and logically parsing it together. I saw a documentary on how difficult this was. Amazing stuff. This is not like neural net black boxes of the past, this is is the start of massive investment portfolios shifting as factors, societal behavioral economics and political change are analyzed by an intelligent program that just keeps getting smarter. If Dalio is doing it, other well-heeled investment managers will pour money into research as well. Where will these programs be in five, ten or thirty years?

Behavioral economics tells us to be humble rather than overconfident for success. Well, a new smartest-guy-in-the-room has arrived so we should take another slice of humble pie. Our thinking around what factors to use and when will be like us trying to beat a Jeopardy champion. Huge hyper-smart portfolios will milk factors and leave few scraps for us. This is another reason that I believe momentum investing is the best factor for the future. It goes with the flow regardless of who or what’s causing the outperformance of the sectors one comes to own.