I haven’t written much about China lately, but I continue to get questions. So I thought that it was time to summarize my big picture thoughts on China here.

Riding a motorcycle at 100mph without a helmet

There is much to cover so I will just go through the highlights. There is no question that the risks are rising in China. The best analogy is someone riding around on a motorcycle at 100mph without a helmet. It doesn’t mean that anything bad happens to you. It just means that if you got into an accident, the results won’t be pretty.

The problems of China are intertwined with each other. The biggest challenge has to do with the buildup of debt to finance unproductive assets. Data from the IMF suggests concern over the level of non-financial corporate debt in China:

While most of the debt remains denominated in RMB and therefore China is unlikely to experience a significant currency crisis in a debt crisis, the global financial system remains vulnerable as recent BIS data shows nearly USD 1 trillion in external foreign currency denominated debt. Note that the data only goes to March 2013 and the reading was USD 880 billion. At that rate of increase, it would not be a big leap to imagine that total external foreign currency debt has topped USD 1 trillion today.

The road gets bumpy

So far, we have a picture of someone riding around on a motorcycle at high speed with little protection. As long as the road is clear and the rider remains in control, everything should be all right. But then the road gets bumpy…

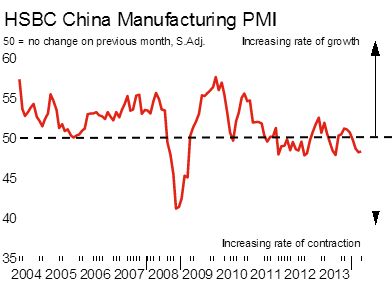

The economy is starting to slow (via Sober Look):

What’s more, FT Alphaville reports that the Chinese property market is starting to soften (emphasis added):

They’re from Nomura’s latest on China property stress which, they say, is increasing at pace. Apparently every property market leading indicator at the national level turned down in Q1, and for most monthly indicators the rate of decline accelerated through the quarter. That, says Nomura, means the question is no longer “if” or “when”, but rather “how much” China’s structurally oversupplied property market will correct.

The greater risk to China lies in the pervasive consequences of any property bust. Property investment has grown to account for about 13 per cent of gross domestic product, roughly double the US share at the height of the bubble in 2007. Add related sectors, such as steel, cement and other construction materials, and the figure is closer to 16 per cent. The broadly defined property sector accounts for about a third of fixed-asset investment, which Beijing is supposed to be subordinating to the target of economic rebalancing in favour of household consumption. It accounts for about a fifth of commercial bank loans but is used as collateral in at least two-fifths of total lending. The booming property market, moreover, has produced bounteous revenues from land sales, which fuel much local and provincial government infrastructure spending.

The reason things look different today is the realisation of chronic oversupply. As the property slowdown has kicked in, housing starts, completions and sales have turned markedly lower, especially outside the principal cities. Inventories of unsold homes in Beijing are reported to have risen from seven to 12 months’ supply in the year to April. But when it comes to homes under construction and total sales, the bulk is in “tier two” cities, where the overhang of unsold homes has risen to about 15 months; and in tier three and four cities, where it is about 24 months.

FT Alphaville reported that declining real estate values can set off a negative feedback loop (emphasis added):

More so, the bet is that the property market is just waaay too important and connected to be allowed to correct aggressively. As ASY says, as property transactions slow, more and more liquidity is trapped in the sector, and this inevitably leads to financial failures and knock-ons everywhere else — downstream industries, local government revenues, collateral for bank lending and via wealth effects on consumption to name a few specifics. As UBS note, given that property investment accounts for almost a quarter of fixed investment, construction value-added is 13 per cent of GDP, and there are extensive linkages between property and industrial sectors including steel, cement and construction machinery, the impact on the economy from a drop in construction volume is bigger than that from a worsening household balance sheet and consumption.

Nomura estimate that property investment (including residential, commercial and public housing) contributes to around 16 per cent of GDP, taking into account its direct contribution and that of related industries such as steel and cement. Not a sector to ignore, in other words, particularly as the property correction could snowball in the short run.

This is the kind of bumpiness in the road that the motorcycle rider will have to navigate.

Building the right kind of road

Instead of worrying about whether the rider will crash, Beijing has opted for a long-term solution of reforming the system to allow China to better deal with shocks – sort of building the right kind of road, so to speak. The leadership in Beijing recognizes the risks to China`s growth model. They have made commitments to reform the system. The latest Five Year Plan calls for re-balancing the source of growth from infrastructure driven growth to consumer driven growth, financial reform and greater mobility from the reform of the hukou system of residency.

These measures sound good, but will it be fast enough and robust enough to forestall a crash? Satyajit Das, who foresaw the global financial crisis but have become a permabear ever since (permabears and permabulls are useful because you always want to hear their side of the story – and they can be right), has warned, despite the rhetoric, that the “’talk-to-walk’ ratio is disappointing”:

In effect, the internal contradictions of an economic model where investment drives growth rather than the reverse will become apparent. Wei Yao, an analyst at French bank Société Générale spoke for many when he termed the effort to balance growth and reform as “mission impossible.”

These tensions may drive a process of ‘skewed reform’. For example, the rapid growth of the shadow banking system constitutes de facto reform of the banking system as depositors can obtain higher returns than that available from banks. But this increases risk. The shadow banking system has led to systemic issues, such as a rapid increase in debt levels and complex links with the banking system. Limited regulation has led to poor governance and risk disclosure. It has increased moral hazard as investors unaware of the real risks rely on state owned banks or governments to ensure return of their capital.

Little is likely to change. At the March National People’s Congress, a meeting to rubber-stamp policies, Premier Li Keqiang conceded as much. While stressing the government was committed to structural reforms, he admitted investment remained “the key to maintaining stable economic growth,” targeted at 7.5%.

The main challenge to these initiatives is Party insiders have become filthy rich prospered under the old system and it would be difficult for them to make changes that hurt their own well being:

Policy implementation will remain challenging. Local governments are unlikely to acquiesce to reforms that undermine their power, which is rooted in rapid growth built around property development using cheap land, mispriced utilities and low taxes. The rebalancing in favor of consumption brings the central government into direct conflict with powerful vested interests that have benefitted from the credit-fueled, investment-based growth model.

As Das puts it, Party insiders will have to gore their own ox in order to implement reforms:

As the process left households and ordinary workers with a relatively small share of GDP, economic rebalancing will require transferring an increasing share to this group at the expense of state-owned enterprises, banks and the economic elite.

In effect, reform requires an implicit redistribution of wealth, encoded in the language of reform — financial market liberalization, reform of state-owned enterprises, and labor mobility. This means that any reform agenda will, in all likelihood, face significant opposition from vested interests in the state sector and local government.

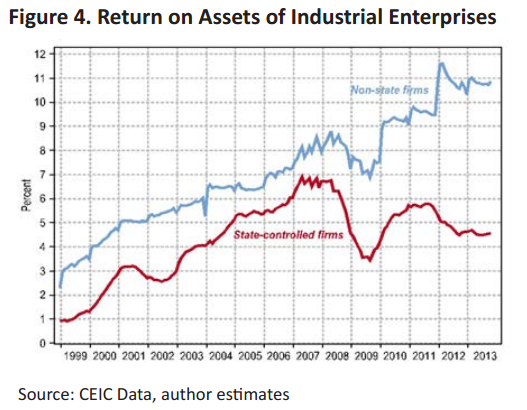

As an example of the difficulties of reforming the state sector, FT Alphaville highlighted analysis from Societe Generale indicating that while the private sector was deleveraging and adjusting to new market realities, the state owned sector continues to add debt:

That chart from SocGen shows that even as the state sector continues to leverage up — among industrial enterprises, the liability-to-asset ratio of SOEs jumped from 57 per cent to 61 per cent between 2008 and 2010, and continued to crawl up afterwards — non-state entities saw the ratio falling all the way from 59 per cent to 56 per cent.

Combine that with a low inflation environment — April inflation data came in notably below expectations and a low inflation environment has persisted for about two years — and a very large negative output gap, you get an argument for a debt-deflation scenario, at least in some sections of the economy.

What about the motorcycle?

I was digressing. All this talk about a building better road is all fine and good, but what about our story of the rider on the motorcycle riding at 100 mph without a helmet?

The most likely scenario is that should the motorcycle rider crash, he will be revived – but as a zombie.

There is a must-read article at Quartz about the outlook for China. It begins with an interview with Patrick Chovanec where he compares China to Japan of the 1980`s. He stated that China is likely to go down the Japanese road. Consider the similarities of Japan then and China now:

Even comparing headline data, the Japan of the 1980s and China of today are strikingly similar:

- Second-largest economy. In 1968, Japan unseated West Germany (paywall) as the second-biggest economy on the planet. China seized that title in 2010, with its nominal GDP of $5.9 trillion nudging past Japan’s $5.5 trillion.

- One-tenth of global GDP. By the early 1990s, Japan’s economy accounted for 10% of global GDP (in purchasing-power parity terms, via the IMF), a milestone China hit in 2007.

- One-tenth of global trade. In 1986, Japan accounted for 10% of global trade, a level China reached in 2010.

- The world’s biggest banks. By the late 1980s, the world’s five biggest commercial banks, by total assets, were Japanese. Here’s how China stacks up now:

The Japanese and Chinese property bubbles are eerily similar:

Banks issue loans off inflated property values

Japanese banks had traditionally loaned against the value of assets, not the income those assets generated; a property deed was considered the most reliable collateral, explains Wood. That policy came in handy as Japan’s capital markets took off. With big companies relying more on the stock market for funding, banks had to find new customers: smaller companies. Less familiar with these new firms, banks used property as collateral for credit. Soaring property values invited bigger and bigger loans. But because property prices had gone up every year since the end of World War II, banks thought their loans were safe.

In China’s case, banks have been issuing loans off not only inflated, but often falsified property values. For real-estate developers and underground bankers, offering real estate as collateral for new loans is a regular practice, says Victor Shih, professor at University of California, San Diego, and an expert on China’s political economy. But “the method of evaluating the collateral is highly convoluted in China so that collaterals are often valued much higher than market-clearing prices,” Shih told Quartz. “As long as banks and other lenders accept such fictional collateral value, they will continue to lend to distressed borrowers.”

If the motorcycle were to crash, the market-oriented policy is to allow the rider to die. The Chinese leadership has been unwilling to embrace that idea and history has shown that whenever the economy slows or shows signs of stress, Beijing capitulates and comes to the rescue and take steps to socialize losses, which would be counterproductive to their goal of reform, because it would be household sector that would ultimately pay the price (see Will Beijing blink yet one more time?). In our motorcycle analogy, it is the equivalent of reviving the corpse and making him into a zombie by lending to and propping up failed enterprises as the Japanese banking system did throughout their Lost Decades.

With China’s stock market already mired in its epic slump, the thing most likely to trigger a Japan-style crisis is a real estate market collapse. However, China already exhibits more than a few symptoms of a zombie infection. Even without the catalyst of a market crash, it in many ways already seems more like Japan in the late 1990s than the Japan of 1989.Though lending continues to surge, it’s getting harder and harder for China to grow. In 2013, credit rose 10% annually (paywall), much higher than the 7.5% expansion of official GDP. That trend is worsening: China must invest twice what it did in 2008 to generate the same amount of GDP growth, according to Wei Yao, an economist at Société Générale. By her tally, China now owes the equivalent of 38.6% of its GDP in principal and interest each year.

Policy makers appear reluctant to embrace the idea of creative destruction. Rather, they would rather live with the zombification of the economy as evidenced by Societe Generale’s above analysis showing that SOEs continued to pile on debt while non-state enterprises were deleveraging (emphasis added):

But growth won’t revive until credit starts supporting the right businesses or industries. Even though state-owned enterprises (SOEs) tend to be much less profitable than private firms, the big banks are also state-owned. And because China’s credit system is still based on political, and not market, risk, the big state-owned banks still loan to SOEs over smaller companies.

That system, says Hoshi, looks awfully familiar. “In a similar way that the Japanese [lending practices] discouraged new entrants… Chinese SOEs are doing the same thing,” he says. “They’re protected, they’re not that profitable, but they can stay in the market because they’re owned by the state, which reduces the possible profit of new entrants.”

Societe Generale (via FT Alphaville) outlined the similarities between SOE zombification and the pushing on a string effects of QE (emphasis added):

If we treat the debt of SOEs and local government guaranteed corporates just as government debt, China’s situation is, to some degree, similar to the post-Lehman US: rising public debt, declining private sector leverage. Particularly, the state sector as a whole generates sub-par economic return. Loss-making industrial SOEs account for more than a quarter of total industrial SOEs, double the ratio among non-state industrial enterprises. Granting credit to profitless corporates is not too much different from having quantitative-easing liquidity trapped in the commercial banks’ vault.

Indeed, Beijing may be in the process of blinking in the face of weakness, despite statements about they will not engage in large scale stimulus programs. Here is Ambrose Evans-Pritchard’s article entitled “China reverts to credit as property slump threatens to drag down economy” (emphasis added):

China’s authorities are becoming increasingly nervous as the country’s property market flirts with full-blown bust, threatening to set off a sharp economic slowdown and a worrying erosion of tax revenues.

New housing starts fell by 15pc in April from a year earlier, with effects rippling through the steel and cement industries. The growth of industrial production slipped yet again to 8.7pc and has been almost flat in recent months. Land sales fell by 20pc, eating into government income. The Chinese state depends on land sales and property taxes to fund 39pc of total revenues.

“We really think this year is a tipping point for the industry,” Wang Yan, from Hong Kong brokers CLSA, told Caixin magazine. “From 2013 to 2020, we expect the sales volume of the country’s property market to shrink by 36pc. They can keep on building but no one will buy.”

The Chinese central bank has ordered 15 commercial banks to boost loans to first-time buyers and “expedite the approval and disbursement of mortgage loans”, the latest sign that it is backing away from monetary tightening.

Longer term, the Quartz article outlined the challenges facing China:

Japan’s experience explains why the challenges facing the Chinese economy are actually much greater even than avoiding a housing market crash or a financial crisis. China’s leaders may well be able to steer the country clear of either. But pulling off yet another miracle of administrative legerdemain will be perilous if it means China’s leaders further postpone financial reforms—things like lifting the deposit-rate cap, allowing SOE failures, or permitting foreign banks to compete. One thing Japan’s history makes painfully vivid is that the longer China waits, the larger its zombie horde grows.

China becomes Japanese

With the Chinese leadership implicitly signaling to the market the existence of a Beijing Put for the Chinese economy, China is unlikely to see a crash landing. The price for such a policy is a prolonged period of slow growth.

In other words, China is likely to turn Japanese. Just don’t tell either the Chinese or Japanese that, they hate each other.

J J J J J

To read more about our writings on China, click here.