So far, so good. The bottom panel of the chart summarizes Scott Bessent’s main challenge in controlling the 10-year yield. The MOVE Index, which is the VIX of the bond market, had fallen since the election and readings are relatively low by historical standards. Bessent’s main task is to calm the bond market and keep anxiety levels low.

Bessent’s tools

Bessent has a number of tools available to him as Treasury Secretary. The first is to signal how he plans to manage the government’s debt. As the Treasury market is the largest and deepest bond market in the world, no government can control it without suffering consequences elsewhere, such as the exchange rate.

The latest Quarter Refund Announcement conveyed a “steady as she goes” message. The expected level of debt issuance is not significantly different than what was a year ago, indicating that Bessent doesn’t expect much progress on the deficit in the near term. In addition, the mix of the issuance of short- and long-term paper was about the same as what it was, despite widespread criticism that the Yellen Treasury was issuing too much short-term paper to boost banking liquidity instead of locking in rates in the longer end of the yield curve.

Bessent’s cautious approach of keeping long-dated Treasury supply relatively low has paid off in the short run, but long-term challenges remain. The non-partisan Congressional Budget Office estimates that fiscal deficits will exceed 5% of GDP for as long as the eye can see — and that assumes the TCJA tax cuts expire. This will put upward pressure on Treasury supply and the 10-year yield as a consequence.

Will supply overwhelm demand under such a scenario? There are some steps the Trump Administration can take to alleviate any potential supply-demand imbalance. Fed Governor Michelle Bowman, who is a front-runner to become the Fed Vice Chair for banking supervision, proposed raising bank leverage ratios in a recent speech:

Where we can take proactive regulatory measures to ensure that primary dealers have adequate balance sheet capacity to intermediate Treasury markets, we should do so. This could include amending the leverage ratio and G-SIB surcharge regulations for the largest U.S. banks. Adopting regulatory changes to mitigate these concerns may not be sufficient to ensure market liquidity, but it would be an important step toward building resiliency in advance of future stress events. In my view, it would be better to fix the roof now, while the sun is shining, by addressing over-calibrated leverage ratio requirements, and considering the unintended consequences of any future capital reforms.

Bowman made a similar suggestion in a speech in January 2024, in the context of addressing possible liquidity problems in the banking system before it occurs:

Looking Beyond Basel III: Leverage Ratio Requirements. Capital requirements are intended to be complementary—risk-based capital rules require banks to hold capital against more granular and specific risks, while leverage requirements operate as a backstop in the ordinary course of business. This arrangement works by design, but we have seen some cracks emerge, particularly around the impact of the 5 percent leverage ratio that applies to U.S. global systemically important banks at the holding company, commonly referred to as the enhanced supplementary leverage ratio (or eSLR). While risk-based and leverage capital requirements are intended to be complementary and promote the safe and sound operation of the banking system, the eSLR can disrupt banks’ ability to engage in Treasury market intermediation, which we saw occur in the early days of market stress during the pandemic. I consider reform of the eSLR to fall in the category of “fixing what is broken.” This is an issue that would be prudent to address before future stresses emerge that could disrupt market functioning.

What does the Fed do?

Even as Bessent focuses on the level of the 10-year yield, which he has no direct control over, he has to contend with the Fed, which controls the short-term rate. Vice Chair Philip Jefferson, who is part of Powell’s inner circle, said in a recent speech that he is in no hurry to cut rates because of the Fed’s data dependence [emphasis added]:

Over the medium term, I continue to see a gradual reduction in the level of monetary policy restraint placed on the economy as we move toward a more neutral stance as the most likely outcome. That said, I do not think we need to be in a hurry to change our stance. In considering additional adjustments to the federal funds rate, I will carefully assess incoming data, the evolving outlook, and the balance of risks

Jefferson’s go slow view was echoed by Dallas Fed President Lorie Logan in a speech last week. She could envisage a scenario in which she wouldn’t support further cuts:

What if inflation comes in close to 2 percent in coming months? While that would be good news, it wouldn’t necessarily allow the FOMC to cut rates soon, in my view.

Suppose, for example, that as the first quarter unfolds, monthly inflation figures come in at a 2 percent annualized rate, labor market indicators hold right where they were all fall, and consumer spending and business investment also stay strong.

I’d find it hard to say monetary policy was meaningfully restrictive in that scenario. One aspect of the global higher-rate environment is that the neutral interest rate appears to have moved up—though it’s uncertain exactly how much. On-target inflation alongside two quarters of stability in the labor market and demand would strongly suggest that we’re already pretty close to the neutral rate, without much near-term room for further cuts. On the other hand, if the labor market or demand cools further, that could be evidence it’s time to ease.

The January Payroll presented a mixed picture. Headline employment came in at 143,000 jobs, which was below the consensus estimate of 169,000, but revisions in November and December added a net 100,000 jobs and the unemployment rate fell from 4.1% to 4.0%. Average hourly earnings spiked in January, but the increase could be related to the cold weather. If sustained, it would represent an unwelcome hawkish development that would put rate cuts on hold. Overall, the report conveyed the picture of a tighter-than-expected labour market.

Trump policy headwinds

Bessent’s desire to maintain a low or stable 10-year yield also faces headwinds from some of Trump’s policies. In addition to the market’s trade war fears, which is a widely shared worry, we have warned in the past about the risks to inflation and economic growth from deportations (see Two Key Risks to the Bull That No One Is Talking About). Both of these issues have drawn increasing concerns on company earnings calls.

Bob Elliott, CEO of Unlimited Funds, highlighted a potential troubling development due to Trump’s strict immigration and deportation policies. Most of the job growth in the latest cycle is attributable to foreign born workers driven by strong immigration, which is about to end.

However, foreigners don’t seem to be pushing out the native-born workers, as the unemployment rates of both groups are very similar.

Not all foreign-born workers are illegal, but if Trump’s deportation policy is sufficiently large in scale, it would remove sufficient people from the workforce to create a worker imbalance and push up wages, which is consistent with Lorie Logan’s scenario of falling inflation and a tight labour market. Moreover, the workforce reduction would put downward pressure on economic growth potential. If labour supply were to stay flat or exhibit weak growth, productivity would have to do most of the heavy lifting if the economy were to grow.

Trump’s widespread use of the tariff weapon is also troubling. When he announced a 25% tariff on Canada and Mexico, a WSJ editorial called it “The Dumbest Trade War in History”. Wall Street strategists all marked up inflation forecasts and marked down growth expectations in reaction to the announcement. Trump acknowledged in a social media post that there may be “some pain” as a result of the tariffs.

As it turned out, the tariff threat to Canada and Mexico was defused, though the China tariffs remain in place. China’s retaliation has been relatively light, unlike the last trade war when China targeted America’s farm exports, which had a widespread impact. This is a constructive sign that China is open to negotiations and not ready to engage in a full-scale trade war.

The verdict

In summary, Treasury Secretary Scott Bessent’s stated objective of focusing on the 10-year Treasury yield is a sensible one, but he faces a number of key challenges.

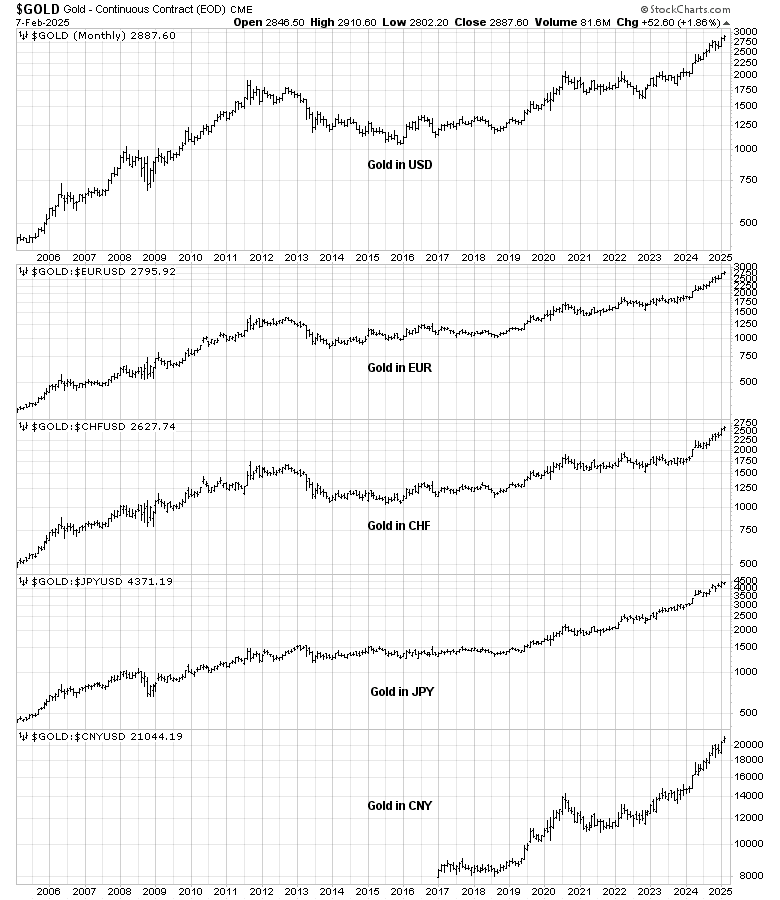

The bears will argue that gold prices, which are a hedge against unexpected inflation, have risen to all-time highs in all currencies.

In the end, much depends on the future trajectory of the term premium, which is the compensation demanded by investors to extend maturity. Any spike in the term premium would pose a serious threat to the success of Trump’s economic agenda, potentially unravel the stability of the Treasury market and crater the appetite for risk assets. Even though the term premium has staged a short and shallow retreat, it remains at a new cycle high and risk levels are elevated.

Cam, this is truly a great analysis, the best have seen among the many I have read. Bessent is the adult in the room. His background is impeccable. This article gives me some small hope we will come out of this era of historic policy change and accompanying chaos without dire consequences. But be clear, I am voting (as in owning) on gold and not 10 Year bonds.

I am just glad that we have now a Prez willing to do unpopular things to make US better. This is necessary for our republic to be viable going forward. I sensed that Americans suddenly have more motivation. It won’t be easy since there are so much entrenched interest which will fight back. Regardless it is a on-going process and for however long it takes to get back to normal we will do it. There is no other alternative. Treat it as a matter of survival. Many very capable people are contributing behind the scene to help. We will start to see some improvement on many fronts. It will be better days.

Could very well see great things eventually happen. Totally agree doing nothing means bad outcomes. I hope for good things but even Musk says there will be pain before the dawn.

What’s going on?

Well, one thing is Federal fiscal deficits, that will almost certainly continue.

How they handle this will have an effect on the market.

If they change the rules on how much federal debt the primary banks hold can they make a variant on what the Bank of Japan did in buying all Japanese debt (or virtually all)?

Does shifting debt maturity more to the short end have benefits beyond a lower rate? It might make for less systemic risk if there are less Silicon Valley banks out there, especially if the ratios for primary dealers are increased and long term bonds get another hit. If you want low risk bonds in an era of possible stagflation that could go on for decades do you want 30 year treasuries? Short term is the way to be safe, a lower yield but less risk to capital.

Bitcoin I don’t believe in, it’s a mania, and just because it keeps going up does not make it a sound investment.

Aside from hacking risks becoming more of an issue with AI are 2 things.

1 is energy cost. According to Hut8 the cost of energy per bitcoin is 30,000$. Yet when there is a halving BTC price goes up because there will be less, only the electric cost per coin just doubled. So yes this would have an effect on the miners making the coin more valuable, but BTC is not like gold. When a gold mine becomes unprofitable it shuts down, and if all gold mines shut down the supply of gold is more or less fixed and the price of gold should go up like art when a famous artist dies. But if BTC miners shut down, you cannot use your coins because you can’t convert them to anything without the miners. If we get at some point a hard landing and things go seriously risk off and BTC prices drop below the electric costs for long enough, how will the miners keep mining since they sell coins to continue mining? Will MSTR dump its holdings in a risk off episode because it is forced to?

Second is the year than no new coins come out. This is a BTC tenet, the supply is limited. Right now at 30k cost per coin the cost is approx 30% of a coin, so in 2037 if you want to use BTC how will this 30% cost be paid for? Service charge? Does anyone want to pay 15% buying and 15% selling the stuff? Maybe, then it would be like buying physical gold or silver where there is a significant buy/sell spread.

Personally, I favor gold and silver and copper because these are useful in an age of electrification, esp silver and gold, but the miners don’t do so well because the cost of mining is so high, but the harder it gets for the miners the more the metals will go up because we really need the stuff.

Technology surprises us, maybe they will find a way to cut the cost of mining dramatically, which would be disruptive. But for now that is not happening.

Look at a monthly chart of GDX:GLD and what is the price doing? It is way down, ditto SIL:SLV. To me this suggests these will become more scarce because mines will shut down even if the resource is not gone but they can’t make enough money to keep the lights on.

Perhaps the casino aspect of explorers would be they way to go, when miners are going out of business the explorers that hit the jackpot should do extremely well, better than in the past.

See comments from Callum Thomas on gold miners

https://bsky.app/profile/topdowncharts.bsky.social/post/3lhnnjysiem2f

Thank you.

This makes me think that if gold prices rise strongly and for long enough, those producing mines could really do well because the cost of building the mine is in the past, so what matters is the operating cost of gold (or whatever one is mining), providing they don’t switch to lower grade ore. Looking at the monthly GDX:$gold chart, we have been more. or less flat. I would look for a breakout to the upside as a signal that owning miners was better than owning gold.