Setting expectations

Fed communications have become far more transparent since the days of the Greenspan Fed. The market interpreted May FOMC meeting statement as a hint at a pause in the rate hike cycle:

In determining the extent to which additional policy firming may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.

The Committee anticipates that some additional policy firming may be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.

The release of the May FOMC meeting minutes revealed a divided Fed, with a tilt toward a pause. On one hand, “some participants commented that, based on their expectations that progress in returning inflation to 2 percent could continue to be unacceptably slow, additional policy firming would likely be warranted”. On the other hand, “several participants noted that if the economy evolved along the lines of their current outlooks, then further policy firming after this meeting may not be necessary”. “Some” is fewer than “several”, right?

I do not expect the data coming in over the next couple of months will make it clear that we have reached the terminal rate. And I do not support stopping rate hikes unless we get clear evidence that inflation is moving down towards our 2 percent objective. But whether we should hike or skip at the June meeting will depend on how the data come in over the next three weeks.

On the other hand, Governor Philip Jefferson, who’s nominated to be Vice Chair and whose views are closer to those of Fed Chair Jerome Powell, said in a separate speech that that hinted at the idea of skipping a rate increase.

A decision to hold our policy rate constant at a coming meeting should not be interpreted to mean that we have reached the peak rate for this cycle. Indeed, skipping a rate hike at a coming meeting would allow the Committee to see more data before making decisions about the extent of additional policy firming.

Arguably, the progress toward lower inflation has been “unacceptably slow”. The April PCE print showed an unwelcome upward surprise in core PCE. In particular, the closely watched super-core PCE, which measures services ex-food and energy and housing, saw the strongest uptick since the start of 2023.

All eyes on the labor market

What will the Fed do? Fed Chair Jerome Powell has acknowledged that goods inflation has been falling, but services inflation remains stubbornly high. He has repeatedly focused on services ex-food, energy and shelter, or “super-core” inflation, as a key metric to watch.

On the other hand, the unemployment rate rose from 3.4% to 3.7%. In addition, MoM average hourly earnings missed expectations at 0.3% and April was revised down from 0.5% to 0.4%, which indicate a weak labor market. As well, average weekly hours fell from 34.4 to 34.3 as a signal of economic weakness.

More crucially, the average hourly earnings of non-supervisory workers, which is less noisy as it excludes the bonuses of managerial workers, showed an unwelcome acceleration.

What’s the Fed’s reaction function?

At the end of the day, making a call on Fed policy is a call on the Fed’s reaction function.

The JOLTS report hasn’t been helpful as a sign that super-core inflation is cooling. The job openings to hires ratio ticked up, and so did the quits to layoffs ratio. The unexpected acceleration in the hourly earnings of non-supervisory workers also did not help matters. The Atlanta Fed’s wage growth tracker is showing stickiness in wage growth. All these signs point to a labor market that remains extremely tight.

All else being equal, further Fed rate hikes will put a bid under the USD, which tends to be negative for risk assets such as equities. In the short run, a negative divergence has been growing between the greenback and the S&P 500. In all likelihood this will create a headwind for equity prices.

Cam

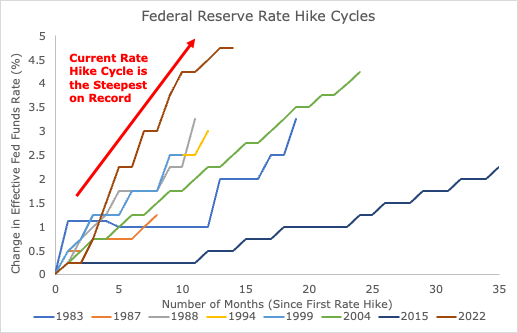

Your last graph says it all. Thanks.